Financing instruments

The regularly-used financial instruments are:

Instrument

Typical providers

Characteristics

Grant

Bilateral donors, philanthropic funds

Provision of funds without expectation of repayment, using government budget allocations, and/or international financial institution/donor funds. An example would be funds provided to pay up-front costs of measures/projects.

Project finance

All of the below

Financing structured around a project’s own operating cash flows and assets, without requiring additional financial guarantees by the project sponsors. Loans in a project finance structure are also called “non-recourse” lending. Project finance depends essentially on the structuring of the risk through risk-cover instruments.

Risk insurance instruments and, guarantees

Export credit agencies, insurance companies, banks, governments, technology suppliers

Insurance instruments provided by either the public or the private sector, in the form of insurance against certain risks and events. Governments will typically provide political (policy) guarantees; private sector entities may provide technical (technology, energy savings) and credit (customer default) risk insurance. Guarantees (non-government) are paid for much like an insurance policy.

Dedicated credit lines

Multilateral and bilateral development banks

Lines of credit (debt finance) for investing in projects that meet specified criteria, e.g. related to climate change. Credit lines are typically established by development banks or less commonly by public entities (government agencies) and channelled through a private sector bank or financial institution for the financing of (most often) private sector initiatives.

Bonds

Financial arrangers such as banks and credit institutions, large corporations, governments

A debt investment in which an investor loans money to an entity (corporate or governmental) that borrows the funds for a defined period of time at a set interest rate. The bond (i.e., the debt) may be traded at an exchange and bought by anyone.

Concessional loans

Bilateral donors (through commercial banks), multilateral development banks

Loans on favourable terms (below market price) with lower interest rates, longer maturities and longer grace periods.

Market-rate loans

Banks, development banks, publicly funded venture funds, pension funds

Traditional debt financing on standard terms (market rate, tenor, grace period), commonly provided by banks, including development banks.

First-loss

Private companies, venture funds, publicly funded venture funds

A tranche of finance that, in the event of a default, takes the first loss, before other tranches. Also called “mezzanine financing” or sometimes “junior debt”. May be regarded as a hybrid of debt and equity.

Equity

Private companies, individuals, venture funds, publicly funded venture funds, pension funds

Investments made directly in projects or operating assets by investors who assume a portion of ownership relative to their provision of capital.

The selection of instruments depends on the viability of the technology being deployed and the market barriers and risks that need to be addressed:

- Concessional loans are generally used for energy transition investments that:

- have high costs for deployment

- cannot compete with existing technologies

- have limited operational experience

- face market and financing barriers that hinder large-scale implementation

- Risk guarantees are an effective mechanism when the commercial financing sources have a perception of high risk with respect to proposed investment. The guarantee reduces this risk perception and facilitates commercial financing

- Market-based loans are used when availability of funds (liquidity) is an issue but there is no need to subsidise the project with concessional financing. These loans help to overcome the liquidity barrier

- Grants are better suited for smaller and focused funding situations, such as financing novel technologies, project development, policy support, capacity building and education. Grant finance is essential for building a pipeline of bankable projects, helping projects reach a level of maturity that might attract investors, and launching pilot projects.

The use of financing instruments is as follows:

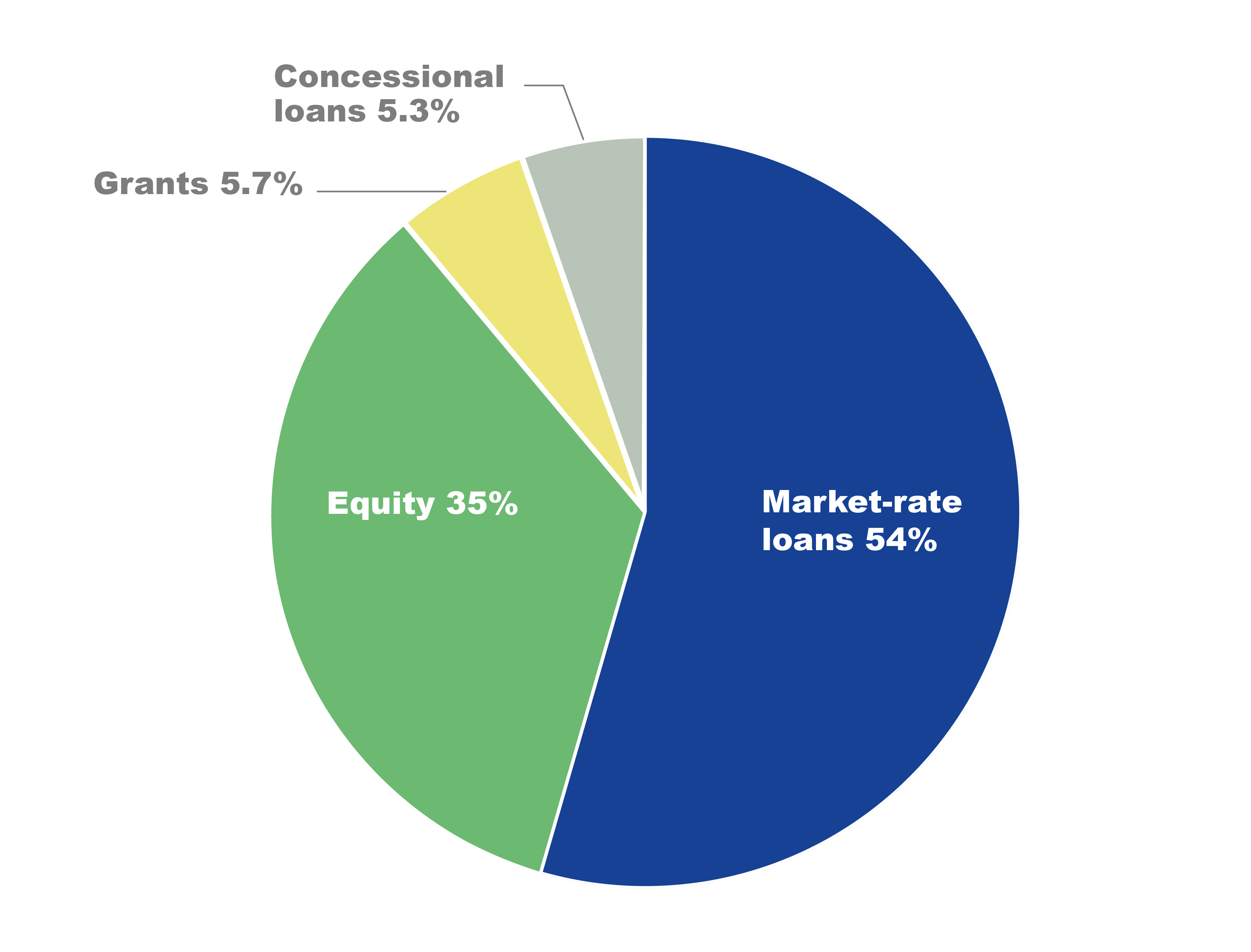

- Loans are the dominant instrument with around 60% of the global climate finance universe

- Within the debt financing segment, market-rate loans command over 90% of all loans provided

- Concessional finance (grants and concessional loans), which is the vital component of climate funding in the developing countries, comprise only 11% of total financing (see Figure 4)

- Scarce concessional finance – most often provided by governments and multilateral, bilateral or national DFIs – is not making its way to less mature markets, which means the energy transition is not able to advance in many developing countries.

Figure 4: Breakdown of global climate finance by instruments in 2022 (total of USD 1,415 billion)

Source: Climate Policy Initiative